Offer in Compromise Guide for IRS & State Settlements

When You Hear About “Settling For Pennies On the Dollar” That’s an Offer In Compromise.

An offer in compromise is one way to settle your taxes owed for less than you owe. To qualify, you must meet strict criteria and provide the IRS with detailed financial information about your assets, liabilitys, and income.

An offer in compromise is one way to settle your taxes owed for less than you owe. To qualify, you must meet strict criteria and provide the IRS with detailed financial information about your assets, liabilitys, and income.

The IRS bases your settlement on your perceived equity in assets along with your income, and if your offer is less than your “reasonable collection potential”, the IRS will not approve it. In other words, the settlement depends on how much you own and earn, and if the IRS thinks it can collect more money from you, it won’t accept your offer.

In recent years, the IRS has rolled back some of the requirements, and as of 2017, the IRS accepts more offers in compromise than ever before. However, acceptance rates are still less than half. To boost your chances of approval, you should work with a tax professional.

Types of Offers In Compromise

There are three main types of offers in compromise:

- Doubt as to collectibility — This is the most common type of offer in compromise. To qualify, you must convince the IRS that you will never be able to pay the taxes owed in full.

- Doubt as to liability — This is where the IRS reduces your taxes owed because there is a doubt that you owe the assessed amount.

- Effective Tax Administration — This applies in cases where you would suffer financial hardship if you paid the full tax bill. Generally, only disabled people and elders qualify for this option.

Filing for an Offer In Compromise Settlement

To apply for an offer in compromise, you need to complete a few forms.

- IRS Form 656 (Offer in Compromise) — Use this form if you are applying for an offer in compromise based on doubt as to collectibility or effective tax administration. The form requests basic information about you. It comes as part of Form 656 Booklet. The booklet contains instructions, Form 656, 433-A, and 433-B.

- IRS Form 433-A (Collection Information Statement for Wage Earners and Self-Employed Individuals) — This form gives the IRS a detailed picture of your financial situation. The IRS uses this information to determine if it should accept your offer or not.

- IRS Form 443-B (Collection Information Statement for Businesses) — This is like IRS Form 433-A but for businesses. If you are requesting an offer in compromise for your corporation, partnership, limited liability company (LLC), or a multi-owner LLC, use this form. To apply for a settlement on both business and personal taxes, you must fill out both the 433-A and 433-B.

- Form 656-L (Offer in Compromise Doubt as to Liability) — If you are applying for an offer in compromise based on doubt as to collectibility, complete this form. In this case, you don’t have to complete Form 433-A or B, but you have to provide supporting documents that show why your taxes owed is incorrect. You also have to make an offer of $1 or more.

Submitting Payment for Offer In Compromise

When you apply for an offer in compromise using Form 656, you must include an application fee and the first payment. As of 2017, the application fee is $186. If you are applying for a lump sum offer, your payment should be at least 20 percent of your offer.

If you are applying for a periodic payment offer in compromise, you must submit your first payment with the application. With a periodic payment plan, you pay the settlement amount over a six to 24 month period. While the IRS reviews your offer, you need to make your proposed monthly payments.

These payments are not refundable. If the IRS rejects your offer in compromise, the IRS will apply the payments to your taxes owed. However, if you send more than the required payment, you can note that the excess amount is a deposit. Then, if the IRS rejects your offer in compromise, you get a refund of that amount.

Note that if you are applying for an offer in compromise based on doubt as to collectibility using Form 656-L, there is no application fee. You also do not have to submit any payments. However, if you do submit a payment, the IRS keeps that amount and applies it to your taxes owed.

Low-Income Certification for an Offer In Compromise

If you qualify for low-income certification, you do not have to make any payments while the IRS reviews your offer. The income amounts to qualify change annually, and the IRS uses different thresholds based on family size and where you live. For example, as of 2017, if you have a family of four and you live in the contiguous 48 states, you qualify for low-income certification if your gross monthly income is less than $5,125.

This only applies to individuals and sole proprietors. To apply for low-income certification, you simply need to check a box on Form 656. If you are applying for an offer in compromise for a corporation, an LLC, a partnership, or another business, there is no low-income certification, and you have to make the required down payment.

Request a Free Tax Analysis & Consult Get Started

Settling State Owed Taxes with an Offer in Compromise

Like the IRS, many states offer settlements on taxes owed, and if you qualify for a settlement on your federal taxes owed, you will probably qualify for a settlement on your state taxes owed. Note that some states use the phrase “offer in compromise”, but others use different names for their programs. To see if your state uses offers in compromise, check out the state tax relief guide page. Each state page explains the settlement methods offered by that state.

Criteria to Qualify for an Offer in Compromise

To qualify for an offer in compromise, you cannot be in the midst of filing bankruptcy. You also must be up to date on your current tax payments such as estimated quarterly payments or sales tax payments. You must have all of your past due tax returns filed as well.

Determining Your Settlement Amount

The IRS requires your offer to be worth the equity in your assets plus your future income minus your allowable living expenses. Here’s a closer look at what the IRS considers in each of these categories.

Assets — If you could sell your assets and cover your taxes owed, the IRS usually won’t accept an offer in compromise. Luckily, when filling out Form 433-A, you only have to account for 80 percent of the value of most assets. Additionally, as of 2017, the IRS allows you to have a bank account balance of $1,000 and a car worth $3,450. You have to note any assets that you have sold in the last ten years on Form 433-A as well as any real property you have transferred in the last three years.

If you have equity in income producing assets that are essential to your business, the IRS usually does not take those assets into account. Additionally, as of 2012, the IRS does not take into account assets you have sold or given away unless that happened six months before your tax assessment.

Future Income Calculation — When determining your collection potential, the IRS looks at your anticipated future income. For lump sum offers, the IRS looks at one year of income. For periodic payment offers, the IRS takes into account two years of future income.

Prior to 2012, when the IRS implemented the Fresh Start Initiative, the IRS looked at four years of future income for lump sum offers and five years of future income for periodic payment offers. This change reduced the average settlement by 60 percent.

Allowable Living Expenses — When determining how much you can afford to pay, the IRS uses a national standards allotment for food, housekeeping supplies, clothing, personal care products, and miscellaneous expenses. As of 2017, a single person gets $639, and a family of four gets a monthly allotment of $1,650 for all of these expenses.

The IRS uses local standards to determine how much you are allotted to spend on housing, utilities, and transportation. The IRS determines the local standards by state and county. Local and state back taxes and federally guaranteed student loans are included as part of your allowable living expenses.

When Your Offer in Compromise Is Accepted

If the IRS accepts your offer in compromise, you need to make your payments as outlined in the agreement. If you qualify for any tax refunds in the year during which your offer is accepted, the IRS keeps those amounts. That money does not go toward your settlement amount. However, if your offer in compromise is for doubt as to liability, you get to keep your refunds or apply them to your settlement.

You also must stay compliant with tax filing and payments for the next five years. If you fail to file a required tax return or make a payment, your offer in compromise defaults.

Once your agreement is approved, you cannot make changes. However, the IRS allows you to make one late payment in a 24-month period as long as the rest of the payments are on time. Once you make all your payments, the IRS removes any tax liens associated with that taxes owed.

When Your Offer in Compromise Is Rejected

If the IRS rejects your offer in compromise, the agency may make a counteroffer. If you don’t want to accept that offer or if the IRS has rejected without making a counteroffer, you have the right to appeal. You must appeal within 30 days using Form 13711 (Request for Appeal of Offer in Compromise).

Why You Should Use a Professional Tax Service For An Offer In Compromise

Get Tax Help

Less than 50 percent of offers get accepted. The IRS rejects the majority of offers because the applicant does not fill out the forms correctly or because the taxpayer doesn’t meet the criteria.

The average tax resolution professional has worked on hundreds of offers in compromise filings, and they know what you need to qualify for particular tax settlements. These professionals have the “IRS formula” figured out. When you work with a professional, your offer is more likely to be accepted, and as an added bonus, a tax professional can help you get a lower offer.

At BackTaxesHelp.com we have a team of tax professionals who specialize in getting offers in compromise accepted. If an offer in compromise isn’t right for you, we can help you find a solution for your particular tax issue. To contact our tax professionals, fill out the form here: Free Tax Consultation.

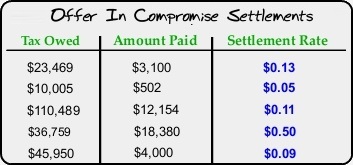

Possible OIC Outcomes

IRS Offer In Compromise Help & Info

Offer In Compromise Help

Do you need help with an Offer in Compromise? Our Partner Tax Team (IRS Agents, Tax Attorneys, Tax Lawyers, CPAs) can ensure proper filing and acceptance by the IRS.

How to Pay Back Taxes

If you do not meet the qualifications for an offer in compromise, it is likely that you will be able to qualify for a different for of payment.

How to Settle Back Taxes

All the available options for settling back taxes. If you don’t qualify for an offer in compromise, you will qualify for some other sort of settlement.

Options When You Cannot Pay Your Taxes On Time

Options for those you can pay a little or nothing to the IRS for back taxes owed. Detail review of each option if you cannot pay your State or IRS back taxes.